GOAL 2017: Global finfish production review and forecast

Farmed fish production continues to increase

This is a summary of some of the findings from the Global Aquaculture Alliance’s survey on finfish species. A presentation of the production estimates, co-authored by Darryl Jory, Ragnar Nystoyl and Ragnar Tveteras, was presented at the GOAL conference in Dublin, Ireland, in October.

The estimates are based on a global survey of many informants undertaken by GAA, which is coordinated by Darryl Jory, and additional estimates from Kontali. Production figures until 2015 are based much on FAO’s Fishstat database. The Norwegian Seafood Council and the U.S. National Marine Fisheries Service has provided data on prices for several species. Table 1 provides a summary of finfish production volumes, and individual species and trends will be further commented in this article.

Global finfish production review and forecast, Table 1

Table 1. Production of surveyed species (regions) in 1000 MT and percentage growth rates.Tilapia

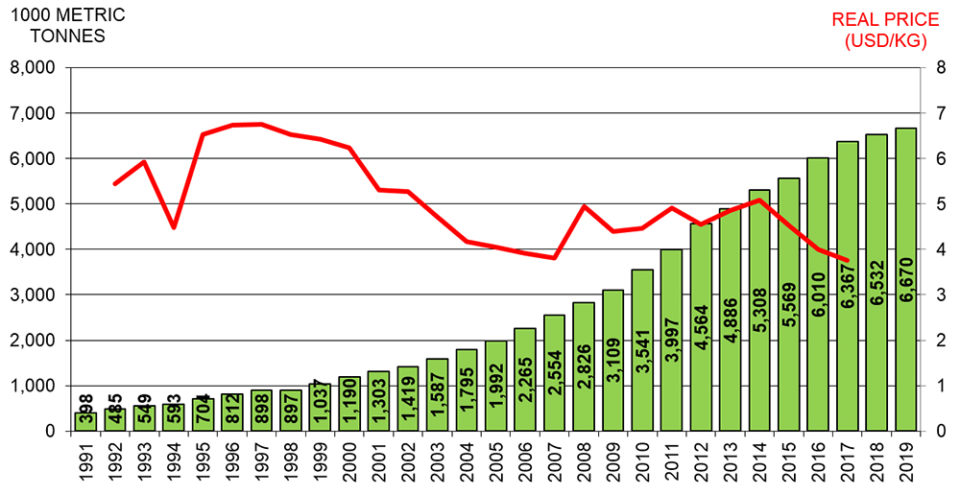

Tilapia, the most diversified species geographically, has continued to add production over time. Production is expected to be around 6.4 million metric tons (MMT) in 2017, a 6 percent growth from 2016. In 2018 production is expected to grow by 2.6 percent to 6.5 MMT. This is still significantly lower than the average growth rate over the 10-year period from 2008 to 2017 period, which has been 9.6 percent.

When we look at a representative price, U.S. import price for frozen fillets, we find that real prices have fluctuated between $4-5 per kg since 2008. It decreased last year to $4, and has on average been $3.75 per kg during the first seven months this year. The substantial increase in production since 2008 has not lead to lower market prices, indicating that the demand for tilapia has also shifted with supply.

China is the leading tilapia global producer, followed by Egypt and Indonesia. For 2017, the average estimate of our sources is 1.7 MMT for China, almost 900,000 metric tons (MT) for Egypt and 800,000 MT for Indonesia. For China, production is expected to be at the same level next year, while for Egypt and Indonesia production is expected to increase.

The range of estimates from different sources on China for 2017 is between 1.3 and 1.9 MMT with an average of 1.7 MMT. For 2018, the range is between 1.2 and 2.0 MMT, also with an average of 1.7 MMT.

Pangasius

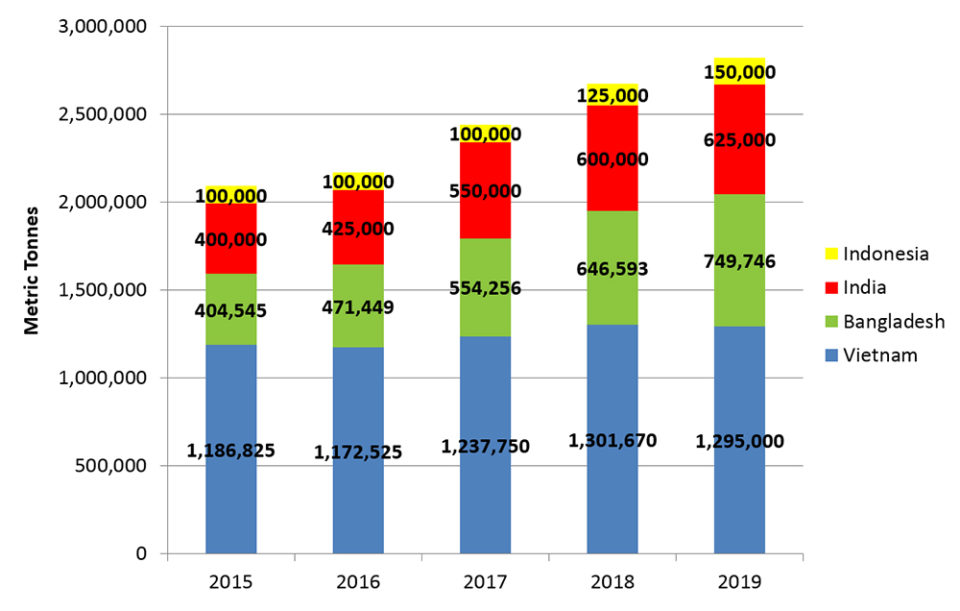

Pangasius is not only a species with a broad market base globally, but its production is also continuing to diversify geographically. Vietnam represents around 50 percent of production among the countries reported here. The total production from those countries reporting is around 2.4 MMT in 2017, as shown in Fig. 2, a 12 percent increase from 2.2 MMT in 2016. Production is predicted to go up by 10 percent in 2018 to 2.7 MMT.

The range of estimates for Vietnam’s production in 2017 is narrow, from 1.2 to 1.3 MMT. When we take the averages of our sources, Vietnam is estimated to experience an increase in production from 2017 to 2018, from 1.23 to 1.3 MMT.

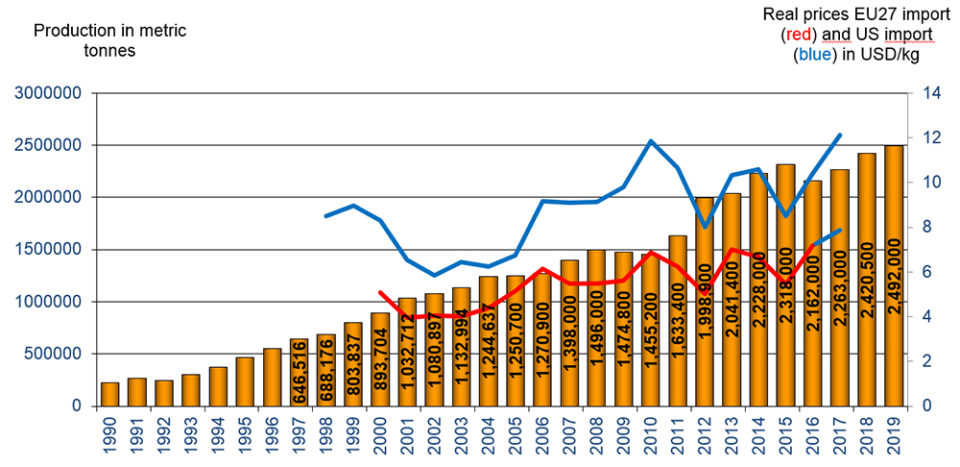

U.S. and EU import prices for pangasius have been declining since 2007, but have stabilized recently. In the first half of 2017, prices have averaged $3 per kg in the United States and around $2.4 per kg in the EU.

Catfishes

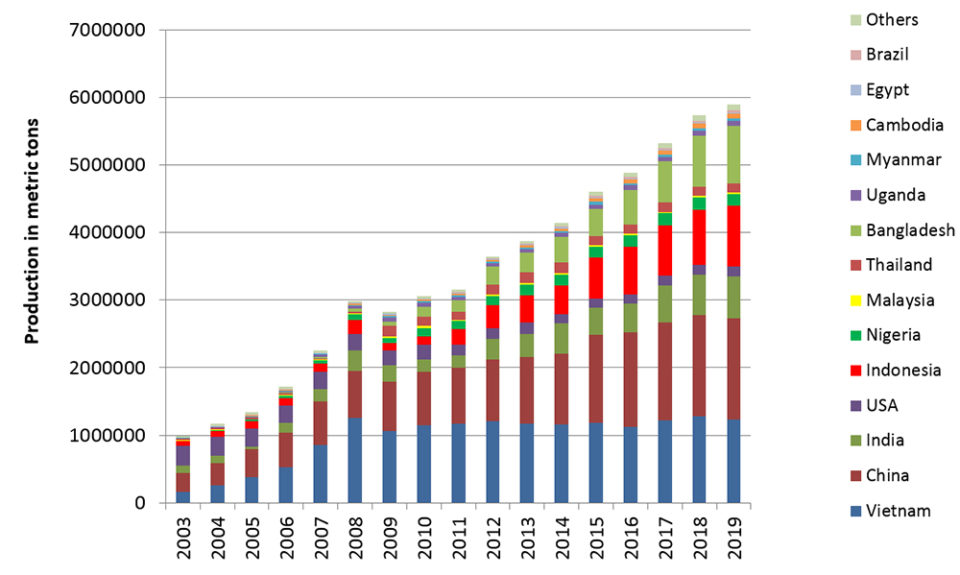

We are still struggling with data coverage for catfishes. As shown in Fig. 3, Vietnam, China, India, Indonesia and Bangladesh are among the largest producers. Total production in those countries we cover has reached levels of 5.3 MMT in 2017, 9 percent higher than the previous year. Production is expected to increase by 8 percent to around 5.7 MMT in 2018.

Salmonids

Atlantic salmon is expected to reach a production of 2.26 MMT in 2017, up by 5 percent from 2016. Prices continued to increase from 2016 to 2017, to $12 per kg for Chilean fillets exported and almost $7.90 per kg for whole gutted salmon into the EU. Prices provide very good margins for efficient salmon producers. Next year, production is expected to increase by 7 percent to 2.42 MMT.

The main producer, Norway, is estimated to have a production of 1.2 MMT in 2017, slightly higher than last year. Chile has experienced a significant increase, from 505,000 MT in 2016 to estimated 546,000 MT this year. Norway is predicted to increase its production by 7 percent in 2018 to 1.3 MMT, while Chile is expected to increase by 9 percent to 600,000 MT.

Coho salmon is a story of ups and downs. Since 2000, Coho production has experienced considerable volatility, fluctuating between 100 and 180,000 MT, but not experiencing any consisten upward trend. Coho production is expected to drop in 2017 to 141,000 MT, down from 147,000 MT in 2016, and next year it is expected to recover to about 166,000 MT. The decline in production in the current year was accompanied by an increase in the export price of Chilean coho frozen fillets, at $6 per kg in the first half of 2017. Chile, by far the dominant producer, is driving the ups and downs of production.

Production of large rainbow trout in marine waters is expected to be around 260,000 MT this year and next, down 7 percent from 281,000 MT in 2015, and well below the peak 2012 level. Prices are up from previous year’s average level, at levels above $8 per kg.

The production of smaller trout, primarily farmed in freshwater, is still on an upward trend. Many countries are involved in the production of small trout, although the neighboring countries of Iran and Turkey together dominate with almost 50 percent of global production. Production is increasing by 5 percent to around 605,000 MT this year. In 2018 production is expected to increase further, by 4 percent to 630,000 MT.

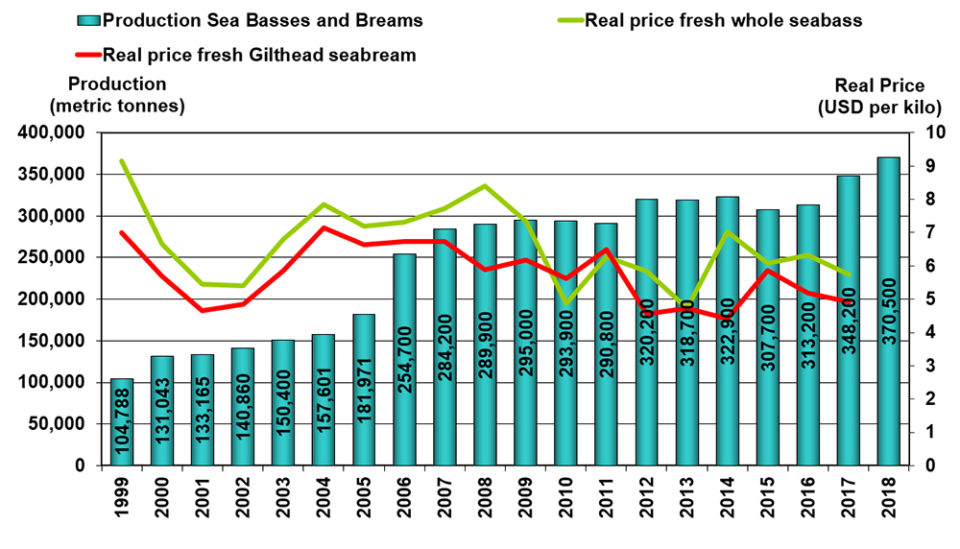

Sea bass and sea bream

Sea bass and bream production in the Mediterranean is estimated to increase in 2017 by 11 percent to around 350,000 MT, as shown in Fig. 5. Next year production is expected to jump by 6 percent to around 370,000 MT. Prices have not provided much incentive to growth, as they have been more or less stable since 2004, and have been declining from 2011 levels. Italian import prices so far this year have been between $6 and $7 per kg.

Other species

We briefly outline developments for other species covered in our survey, with production figures provided in Table 1. Carps are primarily produced for domestic markets. China is by far the dominant producer with around 75 percent of production in 2017 among those carp species and countries covered here. The total estimated production of the sectors included in our survey is around 28 MMT in 2017, up by around 6 percent from the previous year. Next year production is expected to increase by 5 percent to almost 30 MMT.

Barramundi production for the countries covered here is estimated at 84,000 MT in 2017, up by 2 percent from the previous year. Next year the prediction is a further increase of 4 percent to around 87,000 MT.

Cobia production for the countries covered here – China, Taiwan, Panama and Vietnam – is estimated to be 45 MT this year, a decline of 11 percent from previous year. In 2018, production is expected to increase slightly to 48,000 MT. Since 2010, production in these countries has fluctuated around levels of 40 to 50,000 MT.

Turbot production is expected to decrease by 14 percent this year to 111,000 MT, driven primarily by Chinese production. In 2018, production is expected to stabilize at current levels.

Production of bluefin tuna is growing at a rapid pace according to our sources, and is expected to reach 58,000 MT in 2017, up 14 percent from 2016. Next year, production is expected to grow further by 9 percent to around 64,000 MT.

Total production, including carps

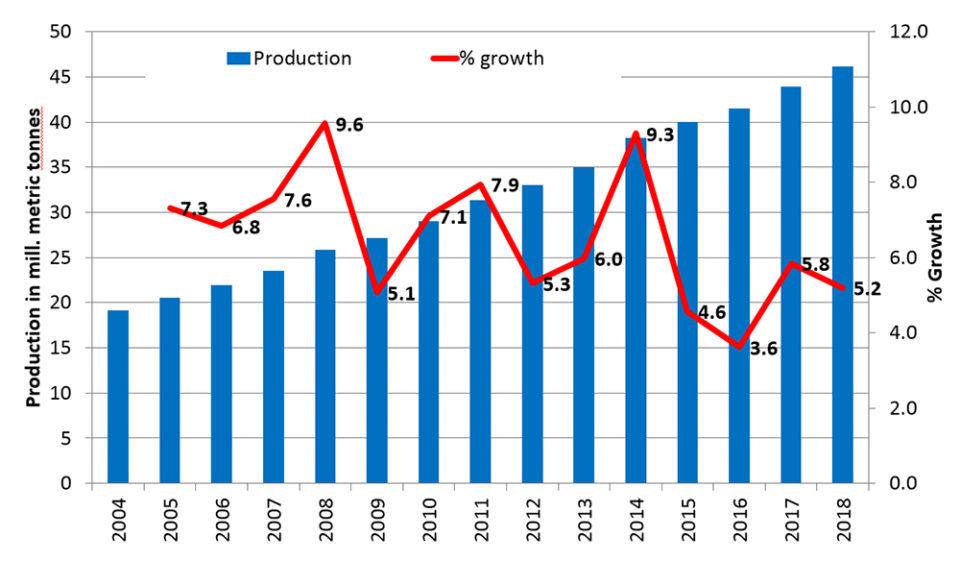

The total production of species and countries covered by our surveys are shown in Fig. 6. In 2015, our surveyed sectors covered 40 MMT of the almost 52 MMT produced in total, according to FAO. We see that production has increased from 19 MMT in 2004 to an expected level of 44 MMT in 2017. Next year, production is expected to be around 46 MMT.

Total production, excluding carps

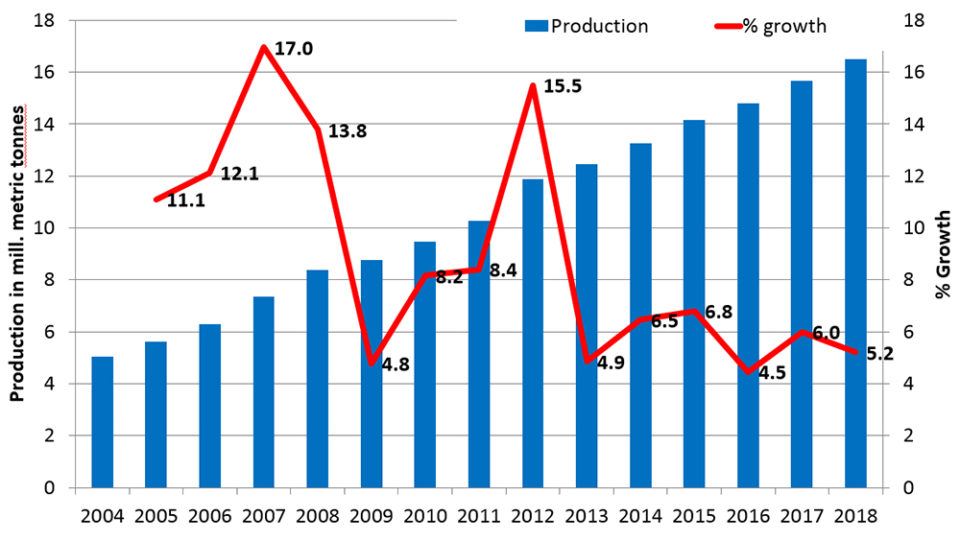

Next, we exclude carps. In 2015 our survey of the remaining fish species covered 14 MMT of the 52 MMT produced globally. We see from Fig. 7 that production of these species has increased from 5.0 MMT in 2004 to 15.7 MMT in 2016.

When we look at growth rates in the same figure, we see a volatile growth pattern. Until 2012, most years have growth rates above 7.2 percent, which is the rate necessary to achieve doubling of production in a decade. But from 2012 growth rates have been in the range 4 to 7 percent. In 2017 the growth rate is expected to be 6 percent, and in 2018 5.2 percent.

Double in a decade?

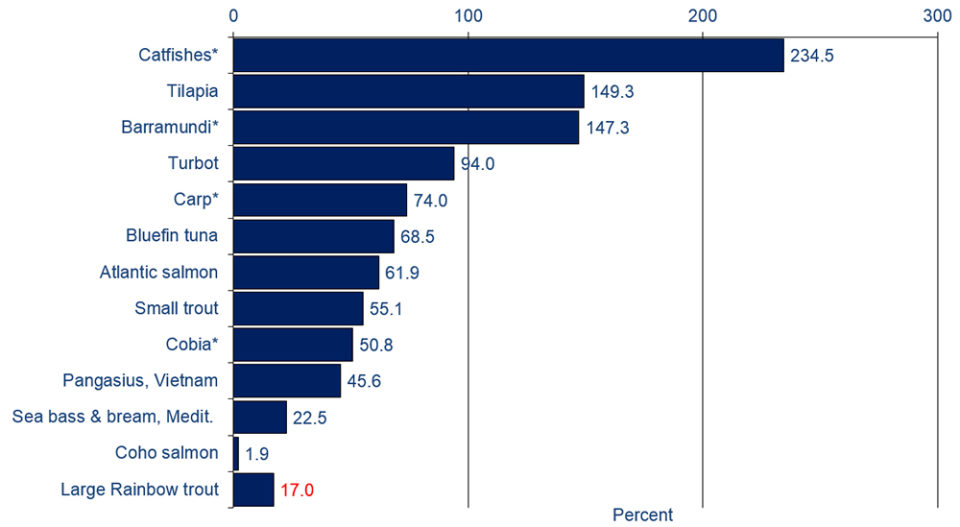

Finally, we determined if the species covered by our survey did double production in the last decade. Fig. 8 shows that the story is mixed at the individual species level. Here we have sorted species by their percentage growth from 2007 to 2017. We see that catfishes, barramundi, and tilapia more than doubled their production.

The remaining species, from turbot and downwards have growth rates below 100 percent. In other words, they have not been able to double production. But still many of these sectors have had very decent growth rates compared with other food producing sectors, and other sectors of the economy in general.

In Fig. 9 we show the percentage growth from 2007 to 2017 for larger species groups and total, and we see a mixed picture. Marine species were not able to double their growth, with a growth rate of 37 percent from 2007 to 2017. Diadromous species increased by 47 percent. Freshwater species increased by 152 percent when we exclude carps. If we include carps in freshwater sectors, they were not able to double, but increased production by 92 percent. The total growth rate when we include carps is at 86 percent. When we exclude carps, we see a more impressive total development, with a growth of 113 percent. In total, the development is fairly impressive, although most of the growth happened in the first half of this 10-year period.

Authors

-

The University of Stavanger

4036 Stavanger, Norway -

Kontali Analyse AS

Industriveien 18, NO-6517 Kristiansund, Norway -

Editor Emeritus

Global Aquaculture Alliance

Related Posts

Intelligence

Global Farmed Finfish Production Outlook: Slower-paced growth

The GOAL 2016 survey for global production of farmed fish shows that most major finfish groups increased their farmed production in 2015. The total production of species and countries covered by the survey is forecasted to reach 42 MMT in 2016.

Intelligence

Global finfish production review: Gradual growth

Recent surveys indicate that global finfish production has doubled over the last decade, but most of this growth happened in the first half of this period. Production is still growing but at slower pace than in recent years, and annual growth rates must increase to at least 7.2 percent to maintain the double-in-a-decade objective.

Innovation & Investment

GOAL 2017 recap: The aquaculture opportunity has hurdles to clear

The great aquaculture opportunity – assuming responsibility as a reliable and predictable source of nutrition for a growing global population – would be better accomplished with a greater sense of confidence, according to keynote speaker Pearse Lyons.

Intelligence

Survey: Salmon can gain a stronger position

With much to learn yet from the more mature chicken sector, farmed salmon has potential to become a more favored option for consumers. This study shows the potential for actions in salmon value chains to improve consumer perceptions.