GOAL 2017: Global shrimp production review and forecast

Shrimp producer surveys generate forecast of 4.82 MMT by 2019

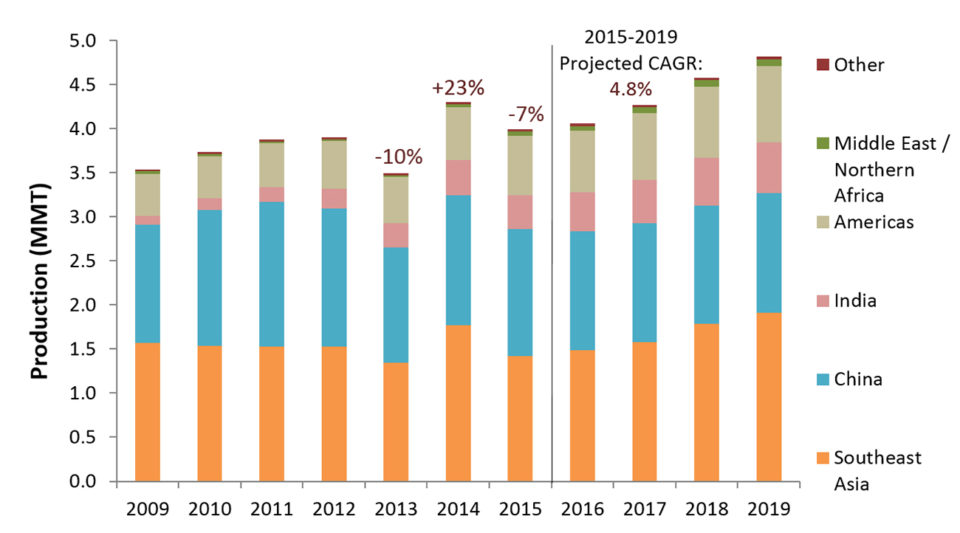

The Global Aquaculture Alliance’s GOAL (Global Outlook for Aquaculture Leadership) 2017 survey of shrimp production trends polled industry participants in Asia/Oceania (43 responses), Latin America (38 responses) and Africa (two responses). Fig. 1 summarizes the production estimates for global production from 2009 to 2019, which combines data from the United Nations Food and Agriculture Organization (FAO) and the 2010-2017 GOAL surveys.

Respondents in the GOAL surveys reported substantial production declines in China, Thailand, Indonesia and Mexico in 2013, following declining harvests in China, Thailand and Vietnam in 2012 related primarily to outbreaks of Early Mortality Syndrome (EMS) that emerged initially in China in 2009.

Surging shrimp prices in international markets during 2013 were consistent with industry expectations of declining production. Nevertheless, FAO data do not reveal any major impact of diseases in Chinese production from 2009 to 2013; on the contrary, China is reported by FAO to have increased production from 1.3 to 1.7 million metric tons (MMT) in this period, growing further to 1.9 MMT by 2015.

In Mexico, FAO reported a 20 percent increase in 2013 even though production had contracted by one half following a major EMS outbreak, according to industry reports.

Given these discrepancies, 2009 data in Fig. 1 were obtained from FAO (2017); 2010 to 2015 data correspond to a mix of FAO and GOAL survey (2011 to 2015) estimates whereas 2016 to 2019 data were obtained from the GOAL 2017 survey. Discrepancies between FAO data and industry reports may narrow in the future as national governments and FAO jointly revise their production statistics.

According to FAO, global shrimp production reached 4.05 MMT in 2011 and then increased to 4.17 MMT in 2012 (up 3.0 percent), 4.30 MMT in 2013 (up 3.2 percent), 4.68 MMT in 2014 (up 8.8 percent), and 4.88 MMT in 2015 (up 4.2 percent). In contrast, the GOAL surveys suggest that world production contracted from 3.87 MMT in 2012 to 3.49 MMT in 2013 (down 10 percent), strongly bounced back to 4.30 MMT (up 23 percent) in 2014 due to improving harvests in China, Vietnam, and Indonesia along with strong growth in India and Ecuador, to fall once again to 3.99 MMT (down 7 percent) in 2015 due to disease problems in virtually all major countries in Asia (Fig. 1).

A minor recovery was estimated for 2016, which is expected to strengthen through 2019, when global shrimp farming production should reach 4.82 MMT (notice that this is slightly less than the global estimate of 4.88 MMT reported by FAO for 2015). GOAL forecasts rely on the expectation that major disease crises are averted in the near future.

Shrimp production in Asia

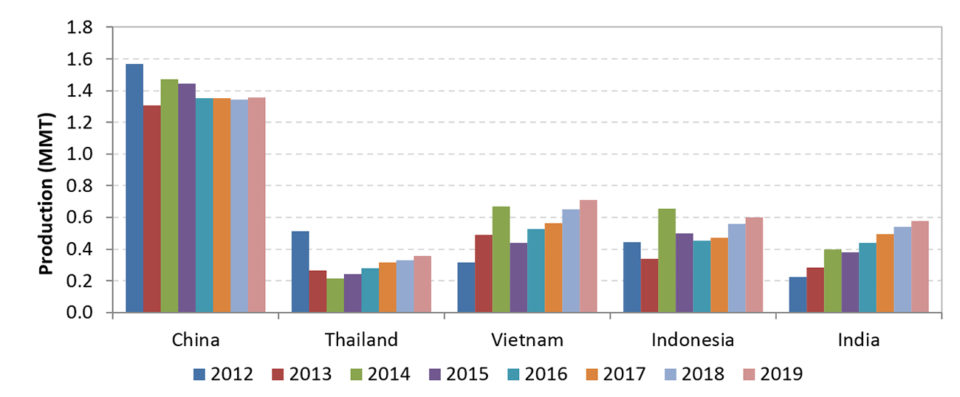

Shrimp production grew steadily in eastern Asia through 2011, with a compound annual growth rate (CAGR) of 5.0 percent from 2008 to 2011. According to GOAL data, production declined from 3.35 MMT to 3.33 MMT in 2012 (down 0.6 percent) and further down to 2.94 MMT in 2013 (down 11.6 percent) due to the impact of EMS in China, Thailand and Malaysia (Fig. 2). Disease challenges have also led to fluctuating production levels in Vietnam and Indonesia. Recovering harvests in China, Vietnam and Indonesia, along with strong growth in India, pushed up production in eastern Asia once again in 2014 (up 24.3 percent to 3.66 MMT), only to see production decline again in most major countries in 2015 (down 10.9 percent to 3.26 MMT).

A recovery led by India, Vietnam and Indonesia began in 2016. Production in China is expected to remain more or less flat at around 1.35 MMT through 2019. Although Thailand is expected to grow at a CAGR of 10 percent between 2015 and 2019 – with production reaching 355,000 MT in 2019 – this recovery would account nevertheless for only 60 percent of the largest production reached during the pre-EMS years. By 2019, Thailand as a shrimp farming nation is expected to remain behind China, Vietnam, Indonesia and India.

The Asia shrimp industry seems to be on the path of recovery following the substantial production declines from 2012 to 2015 caused by pervasive disease outbreaks. Production is expected to reach pre-EMS levels in 2017, driven primarily by growth in Vietnam, Indonesia and India, which on aggregate will grow at a CAGR of 9.4 percent between 2015 and 2019. China will remain the largest producer but its contribution to regional growth will be negligible. Regional production is expected to exceed 3.8 MMT for the first time in 2019. Of course, this set of estimates assumes that no major epidemics will break out in the region in the next few years.

Shrimp production in Latin America

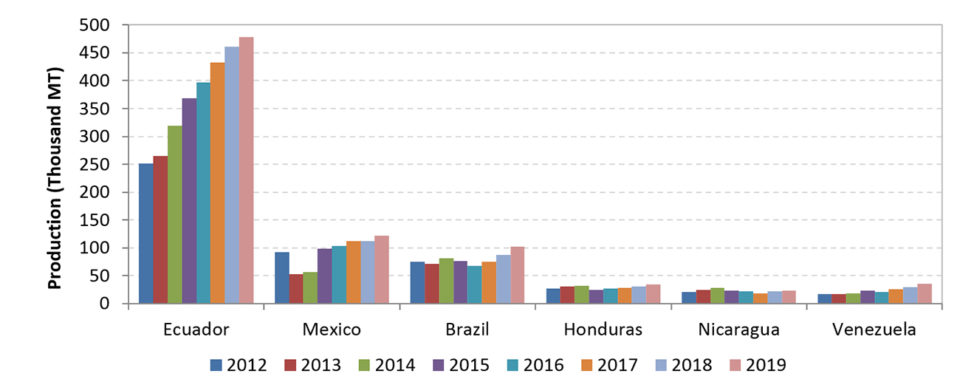

Fig. 3 presents estimates for the major producing nations in Latin America. Besides Asian countries, Mexico was heavily impacted by EMS in 2013: Respondents reported a 44 percent decline in production, from 93,000 MT in 2012 to 52,000 MT in 2013. The industry was nevertheless able to recover output to pre-EMS levels by 2015, with an expected CAGR of 5.2 percent through 2019, when production is expected to exceed 120,000 MT. It is nevertheless noted that this output falls short from the 130,000 MT harvested in 2008.

The most important development in the region is the spectacular growth of Ecuadoran shrimp farming. Ecuador has fully taken advantage of the pervasive disease crisis in Asia to increase exports to European and Asian markets. Production is expected to reach nearly 480,000 MT by 2019, with a CAGR of 6.7 percent between 2015 and 2019. Ecuador will continue to account for more than half of farmed shrimp supply in the Western Hemisphere.

In addition to Ecuador and Mexico, Brazil, Venezuela, Honduras and Panama reported positive expectations for growth through 2019, lifting production in the region from 678,000 MT in 2015 to 868,000 MT in 2019 (CAGR of 6.4 percent). A few other countries such as Nicaragua, Guatemala, Peru and Colombia expect little or no growth due to reasons ranging from the impact of diseases to the reduced potential for expansion of farming areas.

Shrimp product form trends

The GOAL survey also collects information on trends in size categories and product forms. A recent and notable trend in Asia is the increase of green shrimp relative to other product forms such as peeled. While head-on and head-off green shrimp accounted for only 25 percent of production in the 2008 survey, it accounted for 41 percent in the most recent poll. These changes may signal the growing importance of the domestic Chinese market, which prefers green shrimp.

Production in Latin America continues to be oriented towards green shrimp. Head-on shrimp has become the dominant product form over head-off shrimp. It accounted for 56 percent of production in 2016, up from 40 percent in 2007. Increased shipments of Ecuadorian shrimp to European and Asian markets are an important factor driving this trend.

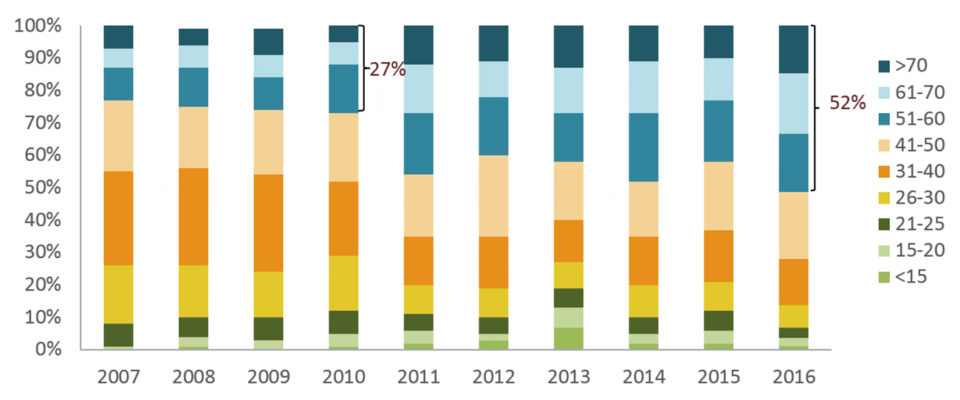

Respondents in Asia have reported a move towards production of smaller shrimp sizes (51-60 and smaller) since 2011 (Fig. 4). The share of small counts increased from 27 percent to 52 percent between 2010 and 2016. The shift to smaller shrimp seems to be driven by narrowing price margins between the small sizes and the larger counts. Early harvests caused by EMS and other diseases also help explain this trend.

Shrimp disease impacts

“Diseases” was once again identified by respondents from Asia as the top challenge faced by the industry. The disease-related issues “Seed stock quality and availability” and “Access to disease-free broodstock” were ranked in the second and third positions respectively, which is consistent with the notion of diseases as the overriding concern in Asian shrimp farming. “Feed costs” emerged as the most important non-disease issue in Asia.

In Latin America, “Feed costs” closely followed by “Diseases” were the top two concerns. “Market prices” completes the set of top three issues for Latin American shrimp farmers.

Perceptions on diseases have changed remarkably over the last 10 years. In the 2007 survey, “Diseases” did not make it among the top three challenges for either Asian or Latin American producers, who used to be more concerned about feed costs, market prices and trade barriers. Disease issues have moved to the forefront in the most recent years, particularly in Asia given the strong impact of EMS.

Most Asian and Latin American respondents expect global economic conditions to either improve or remain stable in 2018; most respondents also expect the global shrimp market to strengthen in 2018. Upward pressure on feed prices is nevertheless expected to continue in 2018.

Authors

-

Director, Institute for Sustainable Food Systems

Professor, Food and Resource Economics

University of Florida

-

Associate Professor, School of Management

University of Los Andes, Colombia

-

Editor Emeritus

Global Aquaculture Alliance

Related Posts

Intelligence

GOAL Shrimp Production Survey: Recovery coming

The GOAL 2015 Shrimp Production Survey showed that global farmed shrimp production is rebounding from the decrease seen from 2011 to 2013 due to diseases, and is headed to an all-time high of around 4.8 million metric tons in 2017, barring any new crises.

Intelligence

GOAL video: James Anderson on shrimp trends

James Anderson delivered a data-rich survey on global shrimp and finfish production volumes for the Global Aquaculture Alliance at its GOAL conference in October. See the full video of his presentation.

Innovation & Investment

20 years of the Global Aquaculture Alliance

A timeline of key milestones and achievements by the Global Aquaculture Alliance and its third-party aquaculture certification scheme, Best Aquaculture Practices (BAP).

Responsibility

A look at various intensive shrimp farming systems in Asia

The impact of diseases led some Asian shrimp farming countries to develop biofloc and recirculation aquaculture system (RAS) production technologies. Treating incoming water for culture operations and wastewater treatment are biosecurity measures for disease prevention and control.